By Dr Graham Brown, Forth Capital

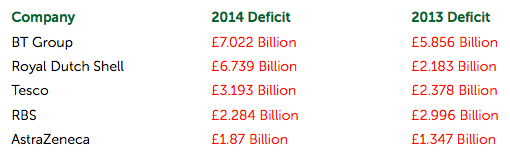

The majority of FTSE 100 Company schemes are in deficit, which is where their pension liabilities exceed their assets and it is clear that the employer does not have the means to make up the deficit in the short term. The numbers are startling according to a Financial Times article on September 7th 2015:

On top of this, approximately 79% of UK defined benefit salary related schemes are in deficit and approximately 60% of that 79% of UK defined benefit salary related schemes have no hope of recovery in the foreseeable future.

As a result, the Trustees may reduce transfer values to be fair to all members. So what happens in the worst possible case?

The Pension Protection Fund (PPF) offers an “insurance scheme” to help provide a minimum level of pension should a pension scheme get into serious financial difficulty. It is funded by a series of levies applied to all final salary pension schemes. It should be noted that the management body of the PPF have the right to reduce the level of compensation being paid from the scheme should the PPF itself suffer financial hardship. The government does NOT underwrite the scheme.

Broadly speaking, those people below the normal retirement age of the scheme when the PPF is appointed will receive 90% of their accrued benefits immediately before the assessment date (subject to a review of the rules of the scheme by the PPF), whilst those past the normal retirement age of the scheme at this date would receive 100% of their accrued benefits.

In the PPF, the total pension is revalued from the PPF assessment date to the normal retirement date in line with statutory orders revaluation. GMP benefits do not receive separate revaluation. Benefits relating to Post April 1997 service will increase in payment (in line with CPI capped at 2.5%), whereas no increase in payment will be made in respect of any pension accrued before 1997.

This compensation is subject to an overall cap (currently £36,401.19 for those retiring at age 65) which will be increased each year, and adjusted to the age at which compensation comes into payment (future increases to the cap are assumed in line with AEI increases).

The PPF is not applicable if your benefits are held within a Public Sector Pension Scheme. This type of scheme is dependent upon income from Local and/or Central Government for its funding. Generally, therefore, a greater degree of security is available.

We suggest that you have your scheme reviewed as soon as possible as it may be better to get out at a reduced value than have the money locked up in the PPF.

Author's bio

Dr Graham Brown has over 30 years’ experience in the Financial Services Industry throughout Asia, the Middle East and Europe. Working for a number of major Financial Institutions including Old Mutual, Credit Lyonnais and Jardine Fleming, Graham has vast experience in managing an array of diverse businesses. Graham joined Forth Capital in 2012 to set up and manage the Hong Kong subsidiary.

Graham specialises in pension transfers, inheritance tax planning and all aspects of personal finances. Having been an expat throughout the last 30 years, Graham has a strong understanding of the expatriate market and an array of personal experience.

Graham is UK qualified, with a Level 4 Diploma in Regulated Financial Planning and is a registered Chief Executive with the Hong Kong Confederation of Insurance Brokers and registered with the Hong Kong Securities and Futures Commission as a Responsible Officer. Graham holds a BSc and PhD in Marine Biology.

Qualifications

- UK FSA Level 4

- HK SFC Investment Adviser

- HK CIB Technical Representative

- HK CIB Chief Executive